Student Loan Interest Rate vs. APR: What's the Difference?

By

ASB

June 29, 2022 |

3 MIN

read

Personal

Resources and content provided by College Ave Student Loans

A student loan interest rate and a student loan annual percentage rate (APR) are similar in that they both represent your cost of borrowing money. There are subtle differences between the two, however, and understanding those differences can impact your student loan decision.

Interest Rate vs. APR: Key Distinction

An interest rate, which is reflected as a percentage of your principal (the amount you borrow) does not include other fees and charges.

An APR includes the interest plus any fees and charges.

That said, different lenders might define an APR – and its associated charges – in different ways. Likewise, many loans have all the above – interest rates, fees, and charges – but some lenders might only list one rate, while others might list both.

This article will dig a little deeper into how student loan interest rates and APRs differ, so you can better assess and compare the true costs of your student loan options.

What Are Student Loan Interest Rates?

An interest rate represents the amount a lender charges you to borrow money. It is calculated as a percentage and multiplied by your principal amount.

Student loan interest rates can be fixed or variable. Fixed rates remain the same for the life of a loan, while variable rates fluctuate with market trends.

With many student loans, interest can start to accrue as soon as your loan is disbursed and will continue to accrue until you repay the loan in full.

What Are Student Loan APRs?

An APR (or annual percentage rate) is meant to serve as an overview of the interest and fees associated with a loan. An APR is therefore often higher than an interest rate.

Additional charges included in an APR might be:

Application fees

Origination fees

Application fees are usually flat fees charged once for completing a loan application. These fees are often non-refundable.

Origination fees are charges associated with processing your loan. They can be calculated as a percentage of your principal or folded into that principal and financed along with it. For this reason, it is important to note that even when a loan’s interest rate and APR are identical, it does not mean your loan is free from additional charges.

Not all lenders charge fees. College Ave Student Loans, for example, does not have any application or origination fees. When you apply for a loan at College Ave, you’ll know your interest rate and repayment terms upfront. This provides a clear picture of the cost of a College Ave loan, which then makes it easier to compare it to other options.

What is Better to Look At – APR vs. Interest Rate?

To get a true assessment of costs, look at both interest rates and APRs. This might require some extra work, but it can save you money in the long run.

It is also important to understand that APRs can differ for federal student loans, in which case the APR might not include a loan’s origination fee.

To ensure you’re shopping for student loans with the right information:

Begin your research early.

Don’t assume the lender with the lowest interest rate is the least expensive option. Ask lots of questions.

A student loan calculator can help you figure out how paying interest while you’re still in school can contribute to saving on your overall loan cost.

When you loan shop from an informed place, you can find and commit to the best student loan for your financial situation.

Resources and content provided by College Ave Student Loans

If you’re thinking about taking out a student loan to help pay for college, you might be navigating the loan process for the first time and encountering a lot of questions, number one on your list being: How do student loans work?

Student loans are a very common and oftentimes necessary way to cover the costs of college. The Institute for College Access and Success has reported that nearly 70 percent of college students nationwide borrow money to help pay for school-related expenses. Student loans make it possible for many people to attend college, which can open doors and opportunities for years to come.

Whether you’re a student or the parent of a student, you’ll want to understand exactly how student loans work, so you can find the student loan that’s right for you.

A student loan is money that you borrow to help pay for school with the expectation that you will pay that money back in the future.

Student loans don’t differ all that much from other types of loans. However, the process of obtaining and repaying a student loan does have some unique attributes.

How Do Student Loans Work?

Your student loan might be the first loan you’ve ever pursued or received, so keep in mind that it’s not just how much you borrow – it’s how much that amount costs in the long term.

Student Loan Interest Rates

One of the most important components of any loan that directly affects its long-term cost is the loan’s interest rate. An interest rate is, essentially, the cost of taking out your loan. It is calculated as a percentage of the amount you borrow and added on to your loan.

A fixed interest rate will not change for the life of a loan, while a variable interest rate can change.

Interest rates for federal student loans, which are issued by the government, are currently set once per year and are fixed. Private student loans, which are issued by banks, credit unions, private lenders, and other types of financial institutions, tend to have interest rates that are higher than federal direct student loans, and those rates can be fixed or variable.

Interest rates will differ depending upon the lender, so this should be a key question as you shop around for private student loans.

Student Loan Origination Fees

You’ll also want to be aware of loan origination fees, which are one-time fees charged when you initially take out your loan. The percentage will vary based on the type of student loan and lender. For federal student loans, the origination fee ranges from 1.057% to 4.228% of the amount you’re borrowing. Many private student loans don’t have origination fees, but that’s not a hard and fast rule.

When charged, an origination fee is usually added to the loan amount, so you typically pay the fee as part of the loan.

Student Loan Repayment Term

Your student loan repayment term is the amount of time you will take to repay the loan. It can vary greatly depending on what type of student loan you take out. Typical repayment terms range from 5 years to 15 years. Be sure you understand what your loan term is before taking out a student loan.

The 2 Types of Student Loans

Students have two main options when it comes to student loans: federal student loans, which are issued by the government, and private student loans, which are issued by nongovernment entities, like banks and other financial institutions.

1. Federal Loan Options

Federal loan options include Direct Subsidized and Direct Unsubsidized Loans.

Direct Subsidized Loans are available to undergraduate students whose families can demonstrate financial need. These are the only federal student loans in which interest does not accrue while the student is enrolled in school at least half-time (or during the grace period following graduation – typically six months).

Direct Unsubsidized Loans are not awarded based on financial need and they are available to most undergraduate and graduate students. Interest will begin accruing at the time of your loan disbursement.

There are annual and lifetime limits for Direct Subsidized and Unsubsidized loans, however, so students might not be able to cover the full cost of college with these federal loan options.

Once a student reaches the limit on Direct Subsidized and Unsubsidized Loans, in most cases they can access Direct Grad PLUS and Parent PLUS Loans.

Direct PLUS Loans have higher interest rates and higher origination fees than Direct Unsubsidized and Subsidized Loans.

2. Private Student Loan Options

Private student loans have different terms depending on the lender. Unlike federal student loans, private student loans typically require applicants to pass a credit and income review to verify that they will be able to repay the loan.

Because most students don’t yet have enough credit history or steady income to qualify on their own, private student loans are often cosigned by someone like a parent or guardian who can meet the criteria and take equal responsibility for repayment. The loan will appear on the credit bureau report for both parties – the student and the cosigner.

Our credit pre-qualification tool allows borrowers or cosigners to find out if their credit qualifies them for a loan, and what interest rates they can expect.

Learn more about cosigners for private student loans.

When Do I Start Paying Back My Student Loan?

Another popular question brought up when on the topic of student loans is “How are student loans paid out?”. Repayment terms on student loans vary based on the type of loan. Federal student loans are often designed to be paid off within 10 years, whereas private student loans might differ based on the lender’s terms.

Students usually won’t have to begin making their federal student loan payments until six months after graduation (or if they drop below half-time status). That said, you always have the option to begin making payments while you’re still enrolled in school.

Many private lenders also offer the option to delay payments until after school, and some, like College Ave Student Loans, offer in-school repayment plans, too. If you can begin making payments during school – even small ones – you’ll usually save money in the long run because you’ll pay less in interest charges.

How Much Will I Owe on My Student Loan Each Month?

This amount will differ for each student based on the amount they borrow and their interest rate. At College Ave, we offer a student loan calculator that allows borrowers to calculate how much their loan will cost and what their monthly payments will be.

Once it’s time to begin making monthly payments, lenders commonly offer the option to enroll in automatic payments, which allows your monthly payment to be regularly debited from your bank account. This can be a convenient option since you’ll never have to worry about missing a payment. As a bonus, you’ll often get a reduction on your interest rate for setting up auto-pay.

If you’re looking to cut down on interest costs, you can always make more than the minimum required payment each month. Even if you’re unable to pay off your loan in full before the repayment period is up, any little bit beyond the minimum can help – especially when you’re talking long-term.

Just be sure your lender won’t charge you a penalty fee if you pay your loan off early. While that type of fee is not common with student loans, it’s always a good idea to confirm.

If You Still Have Questions About How Student Loans Work…

If you have any questions about how a specific student loan works, contact us for clarification before you apply for a student loan. Taking out a student loan is a big decision and how you handle paying it back can affect your credit score. Your credit score can influence future loans and interest rates, so you’ll want to make sure you understand the terms and conditions of your loan before you sign.

If you’re taking on a federal student loan and need more information, you can always reach out to your school’s financial aid office. If you’re shopping around for a private student loan and have additional questions, be sure to contact the lender directly. At College Ave, we offer private student loans that fit your life and your budget.

American Savings Investment Services Wealth Advisors Named 2022 Cetera Circle of Excellence Honorees

By

ASB

May 03, 2022 |

3 MIN

read

News Releases

Three American Savings Investment Services wealth advisors, Angela Chow and Kanani Miyahira were recently named 2022 Cetera Circle of Excellence honorees. The annual prestigious awards event recognizes the accomplishments and leadership of Cetera’s top five percent of advisors in the country for providing comprehensive financial services, including wealth management solutions, retirement plan solutions, advisory services, practice management support, innovative technology, marketing guidance, regulatory support, market research and portfolio analysis.

“With all of the economic uncertainty that’s on the horizon, our experienced wealth advisors are here to guide and provide personalized solutions to help customers achieve their financial milestones,” said Dani Aiu, executive vice president, consumer banking.

The annual Circle of Excellence awards event will be held May 1-5 at the Wailea Beach Resort – Mariott on Maui. Attendees will enjoy a variety of sessions, networking opportunities and speakers.

About the Cetera Circle of Excellence Honorees

Angela Chow, first vice president and wealth advisor, has more than 30 years of experienced in the financial industry. As a Certified Plan Fiduciary Advisor® (CPFA), Chow helps clients understand their risk tolerance and investment objectives, while actively offering portfolio management advice.

“I’m excited to continue serving the Kahala and Kauai communities and I look forward to helping my customers navigate these challenging times and chart a solid financial path forward,” said Chow.

Chow studied finance at the University of Hawaii and Institute of Financial Education and is committed to helping customers reach their financial milestones.

Kanani Miyahira, first vice president and wealth advisor, has over 25 years of experience in financial consulting and investment services. She continues to provide her Pearlridge and Pearl City branch clients with personalized financial solutions tailored to their immediate and long-term goals.

I’m grateful for the opportunity to provide my clients with customized solutions for their investments and other needs,” said Miyahira.

Miyahira received her bachelor’s degree from Oregon’s Pacific University and her MBA from University of Hawaii at Manoa.

Securities and insurance products are offered through Cetera Investment Services LLC (doing insurance business in CA as CFG STC Insurance Agency LLC), member FINRA/SIPC. Advisory services are offered through Cetera Investment Advisers LLC. Neither firm is affiliated with the financial institution where investment services are offered. Advisory services are only offered by Investment Adviser Representatives.

Investments are: Not FDIC/NCUSIF insured • May lose value • Not financial institution guaranteed • Not a deposit • Not insured by any federal government agency

Circle of Excellence: This recognition is not a guarantee of future investment success and should not be construed as an endorsement of the advisor by any client.

Prepare for Rising Mortgage Rates: Tips for Home Owners, Home Buyers and Investors

By

ASB

June 29, 2022 |

3 MIN

read

Personal

Market volatility and rising mortgage interest rates can cause uncertainty for home owners and those looking to buy, but with the right tools, resources and support, American Savings Bank (ASB) can help you achieve your dream of reaching your next financial milestone.

POTENTIAL HOME BUYERS

Home Buying Doesn't Have to be Stressful

Purchasing a home is one of the biggest financial commitments you’ll make and with the right help, it doesn’t need to be a stressful experience. At ASB, we break down the first time buying process with financial wellness courses, mortgage calculators, and seminars so you can feel more confident as you navigate the process.

Visit our Financial Education Center powered by EVERFI for practical tips and helpful resources on maximizing your mortgage, exploring the possibility of an investment property and more.

Select the Right Financing Option

There’s no one-size-fits-all when it comes to mortgage loans, especially in an uncertain market environment. Fixed rate and adjustable rate mortgage loans can offer various benefits when it comes to your monthly principal and interest payments.

Fixed Rate Mortgages offer a fixed interest rate for the entire term of the loan, resulting in an interest rate that does not fluctuate with market conditions.

Adjustable Rate Mortgages offer lower initial payments and an introductory fixed-rate period (often 7 or 10 years). After the fixed period, the rate and monthly principal and interest payments will generally change annually or semi-annually based on the terms of the loan and market conditions.

Compare today’s mortgage rates and take into account your budget, goals and lifestyle when selecting a mortgage financing option. Try our Adjustable-Rate Mortgage Analyzer to get a better understanding of which financing option could be right for you.

EXISTING HOME BUYERS

Use Your Home’s Equity to Pay for Your Biggest Dreams

Congratulations, you’ve secured your dream home! Now what? A home equity line of credit (HELOC) can help you increase the value of your home with a remodeled kitchen or ohana unit for your parents. Use your home’s equity for what’s important to you, including helping your children with a down payment on a new house, upgrading to solar and debt consolidation.

Check out our website for promotional APR and competitive rates and learn more about how a HELOC can help you pay for your biggest dreams!

Mitigate Risk on Your Investment Property

It’s understandable to be concerned about the current market environment and how it will affect your investment property. Here are three tips that can help you reduce your risk:

Make improvements to help your property stand out. In a downturn, your property may not stay vacant for long if it's the nicest on the block. And when the economy is good, you can charge a premium on rent.

Refinance to a 30-year loan. This preserves your flexibility to not pay back the loan in full sooner, and allows you to withstand a vacancy during an economic downturn.

Invest in good insurance. Having good insurance coverage can protect you. Review your current insurance coverage and reach out to your agent about adding an umbrella policy to cover anything above what your current property insurance covers.

Don’t let rising interest rates and an uncertain market environment deter you from making your homeownership dreams a reality. Whether you’re interested in learning more about your current mortgage terms, want to refinance to lower monthly loan payments, looking for ways to increase the value of your home or want to mitigate risks on your investment property, we’re here to help.

Make an appointment with one of our friendly, experienced and knowledgeable bankers today!

NMLS #2358170 Direct: (808) 590-8435 michang@asbhawaii.com Branches served: Hilo, Kailua-Kona, Kapolei and Waipahu, can meet at different branch locations by appointment.

Michael joined American Savings Bank in April 2022. He is committed to helping customers reach their business and financial dreams by offering personalized solutions in commercial lending, small business development and commercial real estate lending. Michael received his bachelor’s degree in finance from the University of Hawaii at Manoa. He brings real impact to the community as a Boy Scouts of America Eagle Scout and also enjoys cooking, surfing and traveling.

NMLS #399228 Direct: (808) 539-7954 chong@asbhawaii.com Branches served: Campus and Main, can meet at different branch locations by appointment.

Christy has more than 20 years of experience in the financial service industry, including wealth management and commercial banking. She is passionate about bringing real impact to our community by supporting local businesses and is committed to helping entrepreneurs navigate the unique opportunities and challenges of running a business in Hawaii. In addition to making customers’ financial dreams possible, Christy is an advocate for supporting women in the workplace through YWCA’s Dress for Success program. In her free time, Christy enjoys international travel and spending time with her family.

American Savings Bank Donates More Than $360,000 to Help Nonprofits and Community Recover From Pandemic

By

ASB

June 15, 2022 |

2 MIN

read

News Releases

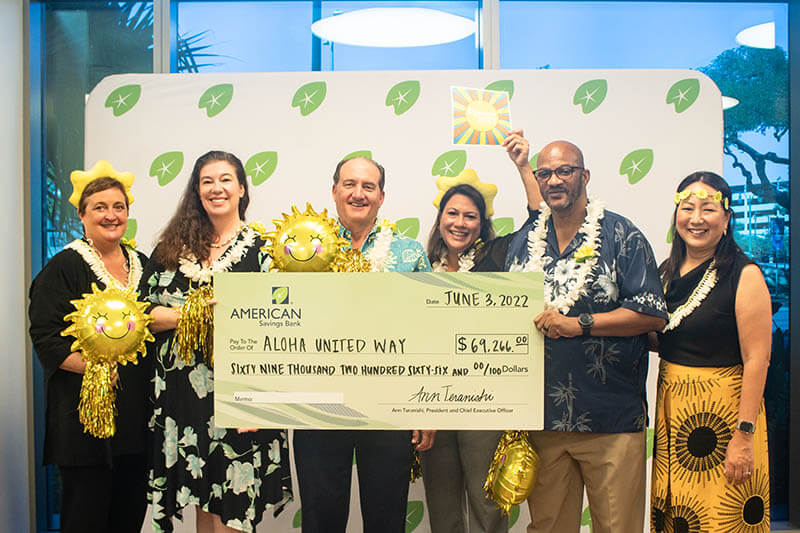

American Savings Bank's (ASB) 2022 Kahiau Giving Campaign raised $362,043, which will allow local community organizations to continue providing critical resources and services to our community. A remarkable 93 percent of ASB teammates participated in the annual workplace giving program, which resulted in the largest Kahiau donation yet.

“Our Kahiau partners have continued to work hard throughout the pandemic to provide much-needed services to our community and we are honored to be able to support them,” said Ann Teranishi, president and CEO of ASB. “I am proud of our teammates’ continued commitment to give from the heart and bring real impact to our community.”

This year’s Kahiau campaign theme was “Here Comes the Sun,” which generated $212,043 in teammate donations. ASB contributed an additional $150,000. As the state continues to recover from the economic effects of the pandemic, ASB teammates remain committed to making dreams possible for customers and the community by bringing sunshine through their donations.

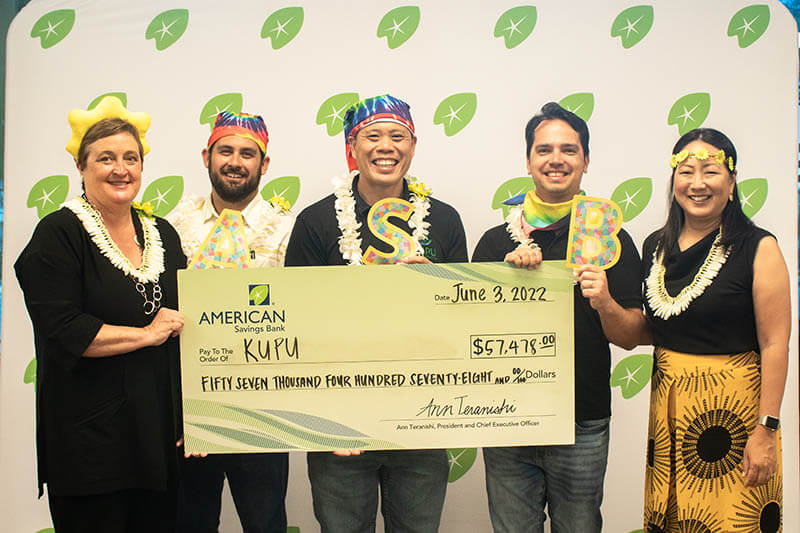

“Working together with like-minded organizations like American Savings Bank helps bring important resources to our youth, community and economy,” said John Leong, CEO of Kupu. “ASB’s support allows us the opportunity to continue preparing future leaders and stewards with a heart for service to people and ʻāina for years to come.”

ASB supports initiatives that promote educational excellence and financial literacy, strengthen families and foster innovation and entrepreneurship through donations, sponsorships, grants, scholarships, internships and volunteerism. ASB supports its Kahiau Community Partners year-round through the bank’s Seeds of Service volunteer program and financial literacy workshops.

“We gratefully applaud the staff and leadership of American Savings Bank as a vital partner in helping us serve low-income, remote, rural families and communities,” said Dr. Shawn Kanaʻiaupuni, president and CEO of Partners in Development Foundation. “Through their support, we continue to provide cultural, trauma-informed educational programs and services across the state.”

Last year, ASB contributed more than $1.5 million to nearly 80 nonprofit organizations and donated more than 13,000 Seeds of Service volunteer hours with nearly 160 nonprofit organizations. In total, ASB has donated nearly 100,000 volunteer hours and millions of dollars to Hawaii’s nonprofits and community organizations, including more than $2.6 million raised through the Kahiau Giving Campaign since 2011.

Aloha United Way: $69,266 donation

Child & Family Service: $95,295 donation

Kapiolani Health Foundation: $97,144 donation

Kupu: $57,478 donation

Partners in Development Foundation: $37,302 donation

NASA Astronaut Visits Hawaii Schools and Teaches Students to Dream Big

By

ASB

May 31, 2022 |

1 MIN

read

Community

NASA Astronaut Dr. Michael Barratt visited three of American Savings Bank’s (ASB) Bank for Education Ohana Schools to talk to students grades K-5 about his career journey and wowed them with inspirational stories about his out-of-this-world experiences as a space traveler.

“We are thrilled to continue this long-standing program that connects students with a real-life NASA astronaut and gives them a behind-the-scenes glimpse into the wonders of outer space,” said Ann Teranishi, ASB president and chief executive officer. “We are committed to supporting local students by providing access to STEM resources that are essential to growing an innovative economy in Hawaii.”

The annual educational event, now in its 22nd year, benefits thousands of Hawaii youth and honors Hawaii-born Astronaut Ellison Onizuka, whose life was cut short on the Space Shuttle Challenger mission. This year marks the 36th anniversary of the Challenger mission.

As Bank for Education Ohana Schools and past KeikiCo Contest winners, Ala Wai, Hokulani and Pearl City Highlands Elementary Schools receive support from ASB through grant awards, financial literacy education and volunteer projects.

Claude Onizuka, Ellison’s younger brother and former ASB branch manager, leads the event that honors his brother’s memory. “My brother once said, ‘Vision is not limited by what your eye can see, but by what your mind can imagine,’” Claude Onizuka said.

Business Lines

Start Your Road to Resiliency Today!

Become Resilient: Obtaining capital or considering technology to help optimize workforce are a few examples of how we can help.

Take Advantage of the Promotion: Secure capital to grow your business by applying for a Business Line today and we will waive your application fee.

We Are Here to Help: Whatever your business goals may be, let us help guide you to grow and manage your business.

Business PowerLineSM

Get access to the funds that you need to keep your business competitive

With Online Banking for Business, you can access account information, transfer funds, deposit checks and more all from the comfort of your place of business or home for free!

You may view your balance in your monthly statement or may access your accounts anytime using Online Banking for Business. Login or enroll in Online Banking here.

Starting Your Business

Find out the best way to start your business with our business insights and planning tools.

Getting pre-qualified for a home loan is a first step in securing your purchase agreement for a property at The Parkways at Maui Lani, located in Kahului. Please contact our Maui lending team for financing solutions and for your free pre-qualification analysis.

150 Hookele Street Kahului, HI 96732 Phone: (808) 627-6900

Paying a Mortgage vs. Paying Rent: What's the Difference?

Taking the path that makes sense for your ‘ohana - especially family finances - is a key ingredient to creating stability and a long-term ability to thrive. So let’s talk mortgage vs. rent....

Folks here in Hawaiʻi might seek out a jumbo loan if they’re thinking about a big single-family home, going in on a multi-family property for the extended ʻohana,...

Mortgage points are one of the most often-referenced (and most confusing) parts of the mortgage conversation. Our expert loan officer has experience making sense of mortgage points and helping families use them as tools....

Thank you for visiting American Savings Bank (ASB). After clicking "I Accept" below, you will transition from ASB's website/application to a third-party's website/application, and agree to waive any claim against ASB that may arise from the third-party's website/application. ASB's privacy policy do not apply to those websites/applications. You should consult the privacy policy of the third-party's website/application for further information. ASB does not provide, and is not responsible for the product, service, or overall content available at third-party websites/applications.