Lawrence Pai

Senior Vice President

Business Banking Director

American Savings Bank

NMLS #639257

Direct: (808) 539-7960

Mobile: (808) 927-1887

lpai@asbhawaii.com

Lawrence brings 35 years of banking experience in the Hawaii market, including 22 years in small business and commercial lending. He is passionate in helping small business owners achieve their business goals, increase their annual revenue, and has garnered many success stories in his long career helping companies grow. He also specializes in helping business owners and individuals purchase small to mid-size apartment buildings and other types of income properties. In recent years, he’s also assisted hundreds of small businesses with the SBA PPP Program. He is a graduate of Pearl City High School, University of Hawaii at Manoa (BBA in Finance), Chaminade University of Honolulu (MBA), and the Pacific Coast Banking School.

.png)

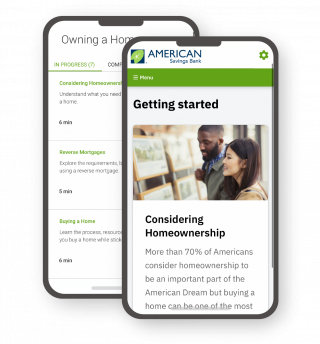

Paying for your share of the rent

Paying for your share of the rent Sending monetary gifts

Sending monetary gifts Collecting money for uniforms

Collecting money for uniforms Splitting the cost of a restuarant bill

Splitting the cost of a restuarant bill Paying for recurring services (e.g. babysitters, landscapers, etc.)

Paying for recurring services (e.g. babysitters, landscapers, etc.) And more!

And more!