What is a Home Equity Line of Credit (HELOC) vs. Refinancing?

By

ASB August 25, 2025 | 5 MIN read PersonalOwning a home is a significant accomplishment for many of us in Hawaii. In addition to that special place where precious memories are made, you can also use your home’s equity to reach your next milestone in life, like creating your dream kitchen or home renovation, to even paying for your kid’s tuition. Read on for more information about how you can use your home’s equity to achieve your financial dreams.

What is Home Equity?

Your home equity is simply the value of your home minus any loans associated with it.

Most banks will allow you to draw from the available equity up to 80% of your home’s value. For example, if your home is worth $800,000, banks may allow you to borrow up to $640,000 ($800,000 x 80% = $640,000). If you already have a $300,000 mortgage on your property, then you may be eligible for an additional $340,000 ($640,000 - $300,000 = $340,000).

As you paydown your loan, each payment reduces your principal balance and increases your home’s equity. The equity in your home will also increase when your home appreciates with the market or through home improvements.

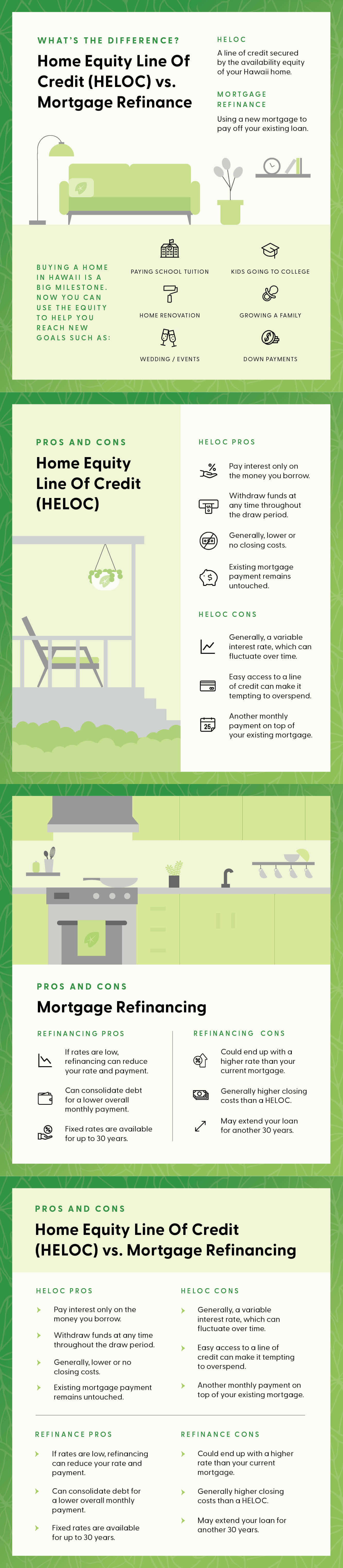

You can tap into your home’s equity through a Home Equity Line of Credit (HELOC) or a cash-out refinance.

What's a HELOC?

A Home Equity Line of Credit, known as a HELOC, is a revolving line of credit based on your home’s equity and works similarly to a credit card but generally, at much lower rates. HELOCs usually have a variable interest rate based on an index, which means as the index goes up or down, so will the interest rate on your HELOC. As an alternative, ASB also offers an option to lock in a low fixed rate on a portion, or all of your outstanding balance.

There’s no interest due on your HELOC until you draw from your line of credit. Once drawn, you’ll only pay interest on that amount during the draw period. For example, if you have a $100,000 HELOC and withdraw $10,000 to pay for a kitchen remodel, you’ll only pay interest on the $10,000. You’re also able to borrow the remaining available balance of $90,000 when needed.

Just like a credit card, you can access your HELOC as much as you need as long as you’re able to pay down the balance to make your credit available again. For example, if you borrow $100,000 from your HELOC and your line of credit limit is also $100,000, you will not be able to borrow from the account again until you pay off all or part of the $100,000 you borrowed, plus interest.

If you are unsure how much money you’ll need, a HELOC gives you the flexibility to draw funds as needed over a 10 year period. After the 10-year draw period ends, you’ll start repaying the outstanding principal plus interest monthly for the next 20 years, unless you choose to pay it off sooner. HELOCs generally have a quicker loan application process with lower closing costs compared to a mortgage loan.

HELOC Pros

You pay interest only on the money you borrow

You can withdraw funds at any time throughout the draw period

You generally will have lower or no closing costs

Your existing mortgage remains untouched, which can be great if it’s at a low rate

HELOC Cons

Generally, a variable interest rate, which can fluctuate over time

Having easy access to a line of credit can make it tempting to overspend

You’ll have another monthly payment on top of your normal mortgage payment when you draw on your HELOC

What's a Refinance?

You may want to consider a cash-out refinance if you don’t want to take out an additional loan on your home. Refinancing your mortgage works by replacing your current 1st mortgage with a new 1st mortgage. Funds from the new mortgage loan are used to pay off the remaining balance on the existing loan and possibly give you more cash. Refinancing is great during times of low interest rates, which can lower your mortgage payment, or to consolidate higher interest credit cards and other loans. A refinance can also help pay off your loan quicker when switching to a shorter-term, such as a 15-year loan.

Most banks will allow you to draw from the available equity up to 80% of your home’s value. Using the same example from HELOCs, if your home is worth $800,000, banks may allow you to borrow up to $640,000 ($800,000 x 80% = $640,000). If you already have a $300,000 mortgage on your property, then you may be eligible for an additional $340,000 ($640,000 - $300,000 = $340,000).

Refinancing Pros

In low-interest rate environments, refinancing can reduce your rate and mortgage payment

Cash-out refinancing can consolidate debt for a lower overall monthly payment

Fixed rates are available for up to 30 years

Refinancing Cons

If current rates are high, you could end up with a higher interest rate than your current mortgage

Closing costs are generally much higher than a HELOC

A refinance may mean extending your loan another 30 years

How to choose between a HELOC or refinance?

Depending on your current mortgage rate and your personal needs, one may be better than the other. If you’ve got a great low rate on your mortgage, it may be best to leave that alone and tap into a HELOC to meet your financial goals. Is there an opportunity to consolidate a lot of other debts like car loans, credit cards, or even an existing HELOC balance? A refinance may be a better option. Check out some of our calculators online or make an appointment with a ASB banker to discuss what’s best for you. Once you’re ready, apply online and you’ll be that much closer to reaching your financial dreams.