APR stands for “Annual Percentage Rate” and represents the price you pay to borrow money. APR is a broader measure than interest rate because it includes the interest rate plus other costs such as lender fees, closing costs and insurance. You can use APR to compare loans offered by different lenders when shopping for a mortgage loan.

For example, based on a purchase price of $500,000; loan amount of $400,000 (20% down payment; 80% loan-to-value); interest rate of 4.00% and 1.00% points, the monthly principal and interest payment on a 30-year fixed rate mortgage would be $1,909.66 and an APR of 4.119%. Keep in mind your mortgage loan monthly payment will be higher as lenders typically include property tax and insurance costs.

Borrower situations vary; contact a loan officer who can provide you with a free analysis.

Make every effort in making your monthly mortgage loan payment on time in accordance to your mortgage and note. If you have an automatic payment set up from a checking account, be sure to have sufficient funds before the date of the debit. If you make your mortgage payment online, be sure to give yourself lead time for the transaction to occur before the due date. If you experience challenges with your automatic payment, your online bill payment, or are unable to pay your mortgage, contact our customer banking center immediately at (808) 627-6900 or our toll-free number at (800) 272-2566 during business hours.

When you bought your home, you likely signed up for the best mortgage loan available at the time. Depending on when you purchased your home and how much income you were earning, you may be on the hook for a large mortgage loan with a high interest rate for many years to come. On the other hand, some Hawaii residents choose to purchase a home using an adjustable-rate mortgage loan. If you bought a home with an ARM, you may be facing variable interest rates that change each year after the initial fixed portion has expired.

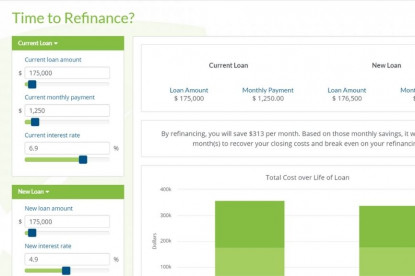

Both of these mortgage loan scenarios might lead you to look into a mortgage loan refinance. As interest rates and family situations change, your mortgage loan for your Hawaii home may not be the best fit for you. A refinance mortgage loan allows you to take advantage of better loan terms or interest rates to pay off the remaining cost of your home. Some other reasons to consider refinancing your mortgage loan include:

- Loan Rates are Down: If Hawaii mortgage loan rates have fallen significantly since you purchased your home, a refinance could potentially save you a lot of money over the life of your loan.

- Your Credit Score is Up: Your credit score plays a big part in the interest rate you receive when buying a home in Hawaii. If your score has increased since you bought your home, you may pay less in interest with refinance mortgage loan rates.

- Interest Rates are Rising and You Have an Adjustable Mortgage loan: With an ARM loan, your interest rate changes according to an index. Usually, this change is done annually, so if interest rates are trending upward, a refinance home loan may be a good option to secure a fixed rate.

- Home Value Increased: If your home value has seen a large increase over the years, you may be able to get additional funds using a cash-out refinance.

There are two main advantages to refinance home mortgage loans in Hawaii with a rate or term refinance. The first is to lower your interest rate. A lower interest rate leads to lower monthly payments and a lower overall cost of the loan. If you use a refinance mortgage loan to lower your interest rate, you could potentially save hundreds or thousands of dollars on the cost of your Hawaii home over the life of the loan.

The second advantage to a refinance is to cut the loan term shorter. If you are able to take advantage of a lower interest rate, you may be able to adjust your monthly payment to pay more money towards the principal of your mortgage loan. This allows you to pay down the remaining balance of your mortgage loan faster.

In addition to advantages from a rate or term refinance, Cash-out Refinance programs have their own unique advantage of allowing you to receive cash for part of the value of your home. Unlike taking advantage of a lower interest rate, a Cash-out Refinance allows you to use the equity you currently have in your home. The additional funds from a Cash-out Refinance can be used for home improvement, investment, or other planned expenses.