APR stands for “Annual Percentage Rate” and represents the price you pay to borrow money. APR is a broader measure than interest rate because it includes the interest rate plus other costs such as lender fees, closing costs and insurance. You can use APR to compare loans offered by different lenders when shopping for a mortgage loan.

For example, based on a purchase price of $500,000; loan amount of $400,000 (20% down payment; 80% loan-to-value); interest rate of 4.00% and 1.00% points, the monthly principal and interest payment on a 30-year fixed rate mortgage would be $1,909.66 and an APR of 4.119%. Keep in mind your mortgage loan monthly payment will be higher as lenders typically include property tax and insurance costs.

Ask your ASB Loan Officer for more information about investment properties and second/vacation homes. ASB has many options to help you add to your real estate portfolio.

If you’re getting ready to purchase a second home in Hawaii, there are many factors to consider. Most importantly, you will want to decide what type of mortgage to use for the purchase. Unlike your first home, you may not be able to take advantage of certain loan programs for a second home. First time home buyer loans, for example, usually require a lower down payment than a conventional loan. However, since you are purchasing a second property, you are unlikely to be able to use a first-time home buyer loan to make the purchase and will need to make a sizeable down payment. The best way to learn what you will need to purchase your second home is to speak with a loan officer with experience in investment properties, like the team at ASB.

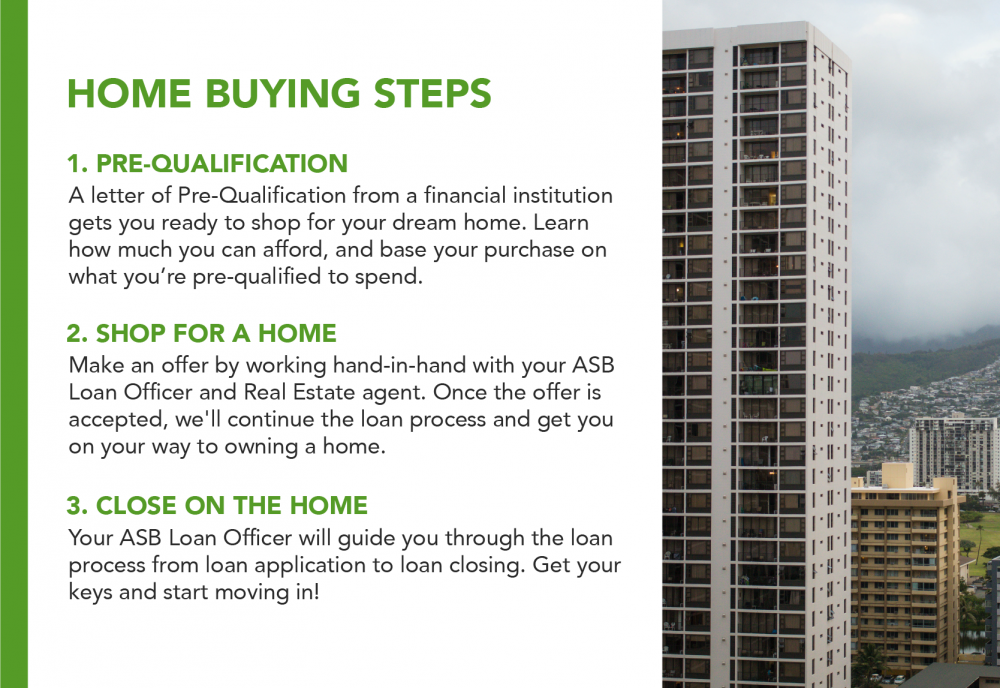

If you’re a first time home buyer in Hawaii, you likely have a lot of questions about finding and applying for your first mortgage loan. Let the mortgage loan experts of ASB help guide you through the home buying process. Your first step to securing the house of your dreams as a first time home buyer is to understand how much you can afford. Consider getting pre-qualified for a mortgage loan so you know how much you might be able to spend on a home.

Start by speaking with the local Hawaii mortgage loan experts from ASB. Our team of knowledgeable loan officers can help you better understand our first time home buyer programs. Whether you decide to purchase your home using a Fannie Mae HomeReady® loan or Combined First and Second Mortgage, our mortgage loan team is ready to help you make your first home purchase in Hawaii.

There are a few items you must consider before applying for a mortgage loan. We recommend that you have a good understanding of how much you want to borrow, what your credit score is, and that your financial information is readily available.

Getting pre-qualified before applying for a mortgage is helpful. Knowing how much of a home you can afford will also help in the house hunting process.

A residential first mortgage is secured by residential real estate property. Therefore, sufficient hazard insurance in case of fire, hurricane, flood and other disasters is required at all times. You must obtain and pay for the premiums if the mortgage is for a purchase of a new home; you must obtain sufficient coverage if the mortgage is for a refinance of an existing home. After mortgage loan closing and the mortgage account is established, an escrow account is used to collect the premiums monthly as part of your mortgage loan payment. A conventional 1st mortgage amount over 80% loan-to-value (LTV) requires private mortgage insurance (PMI), which is paid by the borrower and protects the lender from borrower default on loan payments. PMI cancellation is typically permitted: 1) borrower-requested cancellation, and 2) lender-required cancellation under the Homeowners Protection Act of 1998. For a borrower-requested cancellation, the borrower must provide a written request for cancellation to the lender on the date that the mortgage loan balance is first scheduled to reach 80% of the original value of your home. Certain conditions apply for PMI cancellation.

We typically ask for two years of W-2s and tax returns as well as other documents to verify the information that you provide to us. Every applicant is different, so please contact a loan officer to discuss your situation.