ASB Stories

-

May 15, 2026

Community

May 15, 2026

Community

American Savings Bank Supports Kona Low Storm Recovery Efforts Across Hawaii

As residents and families across Hawaii continue to recover from Kona low storms, American Savings Bank (ASB) is supporting relief and recovery effort...

-

April 06, 2026

News Releases

April 06, 2026

News Releases

ASB Unveils Refreshed Downtown Branch for Easier, More Personalized Banking

Modern 2,600-square-foot space features sustainable materials, open design, and areas for financial conversationsAmerican Savings Bank announced the o...

-

February 02, 2026

Community

February 02, 2026

Community

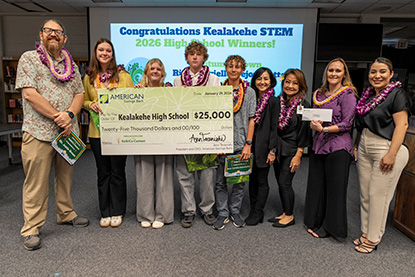

ASB Awards $135,000 to Seven Local Public Schools and Strengthens Financial Literacy for Hawaii’s Future Leaders

American Savings Bank (ASB) awarded $135,000 to nine winning student teams from seven public schools through its annual Bank for Education KeikiCo Bus...

-

January 29, 2026

News Releases

American Savings Bank CEO Ann Teranishi Appointed to Federal Reserve Bank of San Francisco’s Community Depository Institutions Advisory Council

American Savings Bank President and Chief Executive Officer Ann Teranishi has been appointed to the Federal Reserve Bank of San Francisco’s Communit...

-

January 01, 2026

Personal

January 01, 2026

Personal

3 Tips for Buying Your Dream Home in Hawaii

Are you dreaming of owning a home in Hawaii? We’re here to help. At American Savings Bank (ASB), we’re committed to helping you achieve your homeowner...

-

November 14, 2025

News Releases

November 14, 2025

News Releases

ASB's 2025 Workplace Giving Program Contributes $277,000 to Four Local Nonprofits

American Savings Bank (ASB) announced the results of its 2025 Kahiau Giving Campaign, contributing more than $277,000 to four local nonprofits. This y...

-

November 07, 2025

News Releases

November 07, 2025

News Releases

ASB's Hui Kapili Accelerator Receives National Recognition for Tackling Affordable Housing Challenges and Driving Economic Growth

American Savings Bank has received national recognition from the American Bankers Association (ABA) Foundation for its Hui Kapili Accelerator, earning...

-

October 20, 2025

Personal

October 20, 2025

Personal

Avoid Check Fraud with #PracticeSafeChecks Tips and Tools

It should come as easily as fastening your seat belt on a plane, so buckle up for this one. Despite the fact that check use has declined by 25%, repor...

-

October 01, 2025

Personal

October 01, 2025

Personal

Avoid Bank Scams with #BanksNeverAskThat Tips and Tools

At American Savings Bank (ASB), we’re committed to making banking easy and safe for our customers. With October being National Cybersecurity Awareness...

-

August 25, 2025

Personal

August 25, 2025

Personal

What is a Home Equity Line of Credit (HELOC) vs. Refinancing?

Owning a home is a significant accomplishment for many of us in Hawaii. In addition to that special place where precious memories are made, you can al...

-

August 05, 2025

Personal

August 05, 2025

Personal

ASB Opens Applications for 2025 KeikiCo Business Plan Competition

American Savings Bank (ASB) is now accepting applications for its 2025 KeikiCo Business Plan Competition, a statewide challenge that invites Hawaii pu...

-

July 11, 2025

Personal

July 11, 2025

Personal

American Savings Bank Named One of the Best Banks in Hawaii by Forbes for the Sixth Year

American Savings Bank (ASB) has once again been recognized as one of the Best In-State Banks in Hawaii by Forbes – marking six years of this prestigio...

-

July 09, 2025

Personal

July 09, 2025

Personal

Moving to Hawaii? 5 Tips for Purchasing a Property in Hawaii

Hawaii draws new residents from across the country and around the world with its warm beaches, rich and historic culture, and sun-soaked weather. Howe...

-

July 02, 2025

News Releases

July 02, 2025

News Releases

ASB Appoints John Jacobi as Executive Vice President and Chief Information Officer

American Savings Bank (ASB) has named John Jacobi as Executive Vice President and Chief Information Officer (CIO). John will oversee ASB’s technolog...

-

May 08, 2025

News Releases

May 08, 2025

News Releases

ASB and Federal Home Loan Bank of Des Moines Award $625,000 to Six Hawaii Nonprofits to Advance Affordable Housing and Community Resilience

Funding will support programs for Lahaina homeowner recovery, affordable housing, financial education and Aala Park revitalizationAmerican Savings Ba...

-

May 05, 2025

News Releases

May 05, 2025

News Releases

ASB Celebrates Grand Opening of New Lahaina Branch

Fifth Maui location and $10,000 donation to Maui Economic Opportunity demonstrate ASB’s commitment to serving and uplifting Valley Isle communitiesAme...

-

April 15, 2025

News Releases

April 15, 2025

News Releases

Business Leaders Come Together to Equip 12 Local Construction Companies With the Tools Needed to Succeed in Hawaii’s Competitive Market

Experts Say Capacity-Building is Key to Addressing Some of State’s Most Pressing Challengesaio and American Savings Bank (ASB) are pleased to announce...

-

March 18, 2025

News Releases

March 18, 2025

News Releases

ASB Announces 10 Local Nonprofit Winners of $100,000 Community-Driven Competition

Over 24,000 votes cast in support of 30 finalistsAmerican Savings Bank (ASB) is proud to announce the 10 winners of the ASB Charitable Foundation’s $1...

-

February 25, 2025

News Releases

February 25, 2025

News Releases

ASB Celebrates 100 Years of Serving Hawaii with $100,000 Donation to Local Nonprofits

Community invited to vote for organizations to receive funding through March 11To celebrate 100 years of serving Hawaii, American Savings Bank (ASB) i...

-

January 30, 2025

News Releases

January 30, 2025

News Releases

ASB Awards $135,000 to Aspiring Keiki Entrepreneurs

Annual KeikiCo Business Plan Competition is inspiring and developing the next generation of local business leadersAmerican Savings Bank (ASB) awarde...

-

January 27, 2025

News Releases

January 27, 2025

News Releases

Building a Stronger Hawaii: Hui Kapili Business Accelerator Announces Applications for Second Cohort Following Successful First-Year

aio and American Savings Bank (ASB) are pleased to announce the start of the second cohort for the Hui Kapili Accelerator, following incredible succes...

-

January 08, 2025

News Releases

January 08, 2025

News Releases

ASB Celebrates 100 Years of Serving Hawaii’s Residents, Businesses and Communities

Centennial celebration kicks off with announcement of new ASB Charitable Foundation’s $100,000 pledge to local nonprofits.American Savings Bank (ASB...

-

December 31, 2024

News Releases

December 31, 2024

News Releases

American Savings Bank Welcomes New Investors

Bank will continue to operate independently and serve Hawaii’s residents and businesses; no impact to customers, employees or branches.American Saving...

-

December 06, 2024

Personal

December 06, 2024

Personal

Stay Safe This Holiday Season: Tips to Avoid Common Holiday Scams

Information below is provided by the Hawaii Bankers AssociationThe holiday season is a time for giving, celebration, and togetherness – but unfortunat...

-

November 26, 2024

Community

November 26, 2024

Community

ASB Holiday Skateboard Event Inspires Future Skaters at Aala Park

American Savings Bank, Super Skate Posse, APB Skateshop and Trust for Public Land team up with homegrown professional skateboarder Jaime Reyes to brin...

-

October 30, 2024

News Releases

October 30, 2024

News Releases

American Savings Bank Reports Third Quarter 2024 Financial Results

Net interest margin expanded to 2.82%, up 3 basis points from the prior quarterContinued strong credit quality and capital positionAmerican Savings Ba...

-

September 23, 2024

Community

September 23, 2024

Community

ASB Leads Annual Statewide Volunteer Effort for National Cleanup Day

ASB teammates volunteer across five islands to clean and restore Hawaii’s communities and natural environments.Nearly 200 American Savings Bank (ASB...

-

September 04, 2024

News Releases

September 04, 2024

News Releases

Building a Stronger Hawaii: Hui Kapili Business Accelerator Builds Capacity for Local Construction Industry

Sixteen leaders from 10 businesses selected to receive free training, resources and mentorship from industry leaders to elevate their business and the...

-

September 03, 2024

News Releases

September 03, 2024

News Releases

American Savings Bank Pledges $50,000 to Support Rainbow Wahine Student-Athletes

The University of Hawai‘i Athletics Department, in partnership with the University of Hawai‘i Foundation, is proud to announce a new collaboration wit...

-

August 05, 2024

Business

August 05, 2024

Business

Why Every Business Owner Needs a Business Checking Account

Are you starting up a new business? We’re here to help! One of the ways we help businesses manage their finances is by offering different types of bus...

-

July 31, 2024

News Releases

July 31, 2024

News Releases

American Savings Bank Reports Second Quarter 2024 Financial Results

2Q 2024 net loss of $45.8 million reflects after-tax goodwill impairment of $66.1 million in connection with HEI’s ongoing review of strategic options...

-

July 23, 2024

News Releases

July 23, 2024

News Releases

American Savings Bank Opens Applications for 2024 KeikiCo Business Plan Contest

American Savings Bank (ASB) is excited to announce the return of its seventh annual Bank for Education KeikiCo Contest, a business plan competition de...

-

July 17, 2024

Personal

July 17, 2024

Personal

Checking vs. Savings Accounts: Differences Explained

Two of the most popular types of bank accounts are checking and savings accounts come with features that can benefit your financial health. Unsure wha...

-

July 02, 2024

Personal

July 02, 2024

Personal

American Savings Bank Named Hawaii's Best In-State Bank for Fifth Year by Forbes

American Savings Bank (ASB) has been named to America’s Best In-State Banks Forbes Magazine's list of America’s Best In-State Banks 2024 for the fifth...

-

June 20, 2024

News Releases

June 20, 2024

News Releases

ASB and Hawaii Home + Remodeling Launch New Accelerator for Hawaii’s Construction and Building Entrepreneurs

In the midst of a statewide labor shortage coupled with outward migration and a shrinking population due to Hawaii’s high cost of living, Hawaii’s con...

-

May 30, 2024

News Releases

May 30, 2024

News Releases

ASB Donates $443,000 Through Annual Workplace Giving Campaign

American Savings Bank (ASB) is proud to announce that its 2024 Kahiau Giving Campaign has raised $443,000. The charitable contribution will support fi...

-

April 30, 2024

News Releases

April 30, 2024

News Releases

American Savings Bank Reports First Quarter 2024 Financial Results

1Q 2024 Net Income of $20.9 million, an increase of 12.8% from 1Q 2023Strategic Balance Sheet Repositioning Executed in the Fourth Quarter of 2023 Con...

-

April 03, 2024

News Releases

April 03, 2024

News Releases

ASB and Federal Home Loan Bank of Des Moines Award $850,000 to Six Hawaii Nonprofits

American Savings Bank (ASB) and the Federal Home Loan Bank of Des Moines (FHLB Des Moines) are pleased to award $850,000 to six local nonprofits throu...

-

March 12, 2024

Community

March 12, 2024

Community

ASB Reaffirms Its Commitment to the Community With Highest Annual Charitable Giving Amount in Company History

Despite another challenging year for the banking industry, American Savings Bank (ASB) exceeded its 2023 annual charitable giving goals, driven partly...

-

March 05, 2024

News Releases

March 05, 2024

News Releases

Brad Mattocks Joins ASB as Executive Vice President and Chief Information Officer

American Savings Bank (ASB) has hired Brad Mattocks as its Executive Vice President and Chief Information Officer (CIO), following the planned retirem...

-

January 30, 2024

Personal

January 30, 2024

Personal

Banking Basics for Teens

PICTURE THIS: You’re about to start a summer job and your boss asks you for your bank information so you can deposit your paycheck right into your ban...

-

January 30, 2024

Other

January 30, 2024

Other

The 411 on the Earned Income Tax Credit (EITC)

Note: This post shares information relevant to tax filers. Consult your tax advisor for information regarding your individual situation.Have you heard...

-

January 30, 2024

News Releases

January 30, 2024

News Releases

American Savings Bank Reports Fourth Quarter and Full Year 2023 Financial Results

Full Year Net Income of $53.4 Million2023 Results Include an $11.0 Million After-tax Loss Resulting from a Fourth Quarter Balance Sheet Repositionin...

-

January 08, 2024

News Releases

Tony Mizuno Promoted to Executive Vice President of Commercial Banking Following Gabe Lee's Retirement After 25 Years at ASB

American Savings Bank (ASB) announced the retirement of Gabe Lee, who served as Executive Vice President (EVP) of Commercial Banking for over 25 years...

-

December 28, 2023

Community

December 28, 2023

Community

Guy Fieri Foundation Donates $1.2 Million to Lahaina Restaurant Workers Impacted by Wildfires

With a deep love for Maui, celebrated chef and TV personality Guy Fieri teamed up with the Hawaii Restaurant Association (HRA), American Savings Ban...

-

December 26, 2023

Community

December 26, 2023

Community

ASB Awards Over $145,000 to Winners of KeikiCo Business Plan Competition

Student entrepreneurs across the state presented their best ideas in American Savings Bank’s 6th annual Bank for Education KeikiCo Business Plan Compe...

-

December 01, 2023

Community

December 01, 2023

Community

Keiki Super Skaters Fly High at Aala Park

On Sunday, Dec. 3, American Savings Bank (ASB), Super Skate Posse, APB Skateshop and Trust for Public Land join forces at Aala Park for a sneaker, hel...

-

November 08, 2023

News Releases

American Savings Bank Reports Third Quarter 2023 Financial Results

$8.6 Million of Maui Wildfire-Related Expenses, Including $5.9 Million of Additional Provision. Solid Credit Quality and Capital Position. Liquidity R...

-

October 30, 2023

Personal

October 30, 2023

Personal

What is a Home Equity Line of Credit (HELOC), and is it Right for Me?

A HELOC is a line of credit that allows homeowners to borrow against the equity in their home. A HELOC is like a credit card, giving you the flex...

-

October 28, 2023

Community

October 28, 2023

Community

ASB's Annual Statewide Volunteer Day on Five Islands Makes a Significant Impact on National Make a Difference Day

American Savings Bank (ASB) brought together hundreds of teammates, friends and family members across five islands on Saturday, Oct. 28, in honor of N...

-

September 01, 2023

Personal

September 01, 2023

Personal

American Savings Bank Receives Exceptional Community Bank Service Award

Content written by Independent BankerThere’s a word in Hawaiian—kahiau—that means to give generously without expecting anything in return, and America...

-

August 22, 2023

News Releases

August 22, 2023

News Releases

American Savings Bank Reaffirms Strong Capital Position, Excellent Credit Quality and Ample Liquidity in Aftermath of Maui Wildfires

American Savings Bank (ASB), is well positioned and stands ready to support the community as families heal and rebuild in the aftermath of the Maui wi...

-

August 10, 2023

News Releases

August 10, 2023

News Releases

Hawaii Bankers Association Member Banks Accepting Monetary Donations to Support Maui Relief Efforts

The Hawaii Bankers Association (HBA) announced today it launched Aloha for Maui, a program accepting donations at any of its member branches statewide...

-

August 09, 2023

News Releases

August 09, 2023

News Releases

American Savings Bank Pledges $100,000 to Wildfire Relief Efforts

American Savings Bank (ASB) committed to donate $100,000 to nonprofits, including the American Red Cross, to provide assistance to local residents and...

-

August 04, 2023

News Releases

August 04, 2023

News Releases

American Savings Bank Opens Registration for 2023 Bank for Education KeikiCo Contest

American Savings Bank (ASB) is excited to announce the return of its Bank for Education KeikiCo Contest, an annual business plan competition that empo...

-

July 18, 2023

News Releases

July 18, 2023

News Releases

ASB Launches “This is HOME” First Time Home Buyer Program to Address Growing Housing Crisis

American Savings Bank (ASB) is proud to introduce “This is HOME,” a new first-of-its-kind affordable financing solution for first time home buyers des...

-

July 12, 2023

Personal

July 12, 2023

Personal

American Savings Bank Named Best Bank by HONOLULU Magazine

American Savings Bank (ASB) was recently voted a Best Bank in HONOLULU Magazine’s “Best of HONOLULU” list.The annual “Best of HONOLULU” award list cel...

-

June 21, 2023

News Releases

June 21, 2023

News Releases

ASB and Federal Home Loan Bank of Des Moines Award $1.8M to Local Nonprofits

American Savings Bank (ASB) and the Federal Home Loan Bank of Des Moines (FHLB Des Moines) are proud to announce the award of $1.8 million to eight lo...

-

June 20, 2023

News Releases

June 20, 2023

News Releases

American Savings Bank Named Hawaii’s #1 Best Bank in Forbes 2023 List

American Savings Bank (ASB) has been recognized as the only bank in Hawaii named on Forbes’ America’s Best-In-State Banks 2023 list. This prestigiou...

-

May 30, 2023

Personal

May 30, 2023

Personal

Buying a Condo in Hawaii: What to Think About When Purchasing Your Vacation Home

Sparkling blue water, soft sand beaches, and exciting local culture make Hawaii a go-to destination for vacationers from around the world. Maybe you’v...

-

May 24, 2023

News Releases

May 24, 2023

News Releases

ASB and Fiserv Award $10,000 to Local Business in Molokai

American Savings Bank (ASB), in collaboration with Fiserv, Inc., is proud to announce the recipient of a $10,000 grant as part of the Fiserv Back2Busi...

-

May 23, 2023

News Releases

May 23, 2023

News Releases

ASB Invests More Than $4.3 Million in Hawaii Community Lending

American Savings Bank (ASB), in collaboration with Hawaii Community Lending (HCL), announced the bank’s $4.3 million investment in homeownership oppor...

-

May 22, 2023

News Releases

May 22, 2023

News Releases

ASB Donates More Than $368,000 to Support Local Nonprofits Addressing Critical Community Needs

American Savings Bank (ASB) is proud to announce that its 2023 Kahiau Giving Campaign has raised $368,268, which will enable local organizations to co...

-

May 02, 2023

News Releases

May 02, 2023

News Releases

ASB Hosts Seeds of Service Community Clean-Up

American Savings Bank (ASB) partnered with more than 20 organizations to bring real impact to the community through its Seeds of Service Community Cle...

-

April 21, 2023

Personal

April 21, 2023

Personal

ASB Named Best Place to Work in Hawaii for 2023

American Savings Bank (ASB) has been named a Hawaii Business Magazine Best Place to Work for 2023, now totaling 14 consecutive years of ASB receivin...

-

April 13, 2023

Personal

April 13, 2023

Personal

What is a Certificate of Deposit and What Are its Pros and Cons?

Savings accounts aren’t the only option you have when saving for the future. A Certificate of Deposit (CD) can also help you reach your goals. CDs com...

-

April 13, 2023

Personal

April 13, 2023

Personal

Emi Au Named 2023 Women Who Mean Business Honoree

Emi Au, Senior Vice President, Director of Consumer Banking Strategy and Planning, was recently named a Pacific Business News (PBN) Women Who Mean...

-

April 10, 2023

Personal

April 10, 2023

Personal

Jumbo Loan Options: What to Know About Terms and Rates

In Honolulu County, as in many neighborhoods throughout the islands, more than half of the single-family homes hover near a million. If your family is...

-

April 06, 2023

News Releases

April 06, 2023

News Releases

ASB Introduces New Mortgage Options to Expand Affordable Homeownership Access for Native Hawaiians

American Savings Bank (ASB) is now approved by the U.S. Department of Housing and Urban Development (HUD) to provide HUD 184A and FHA 247 loans to the...

-

April 04, 2023

News Releases

April 04, 2023

News Releases

ASB Releases First Environmental, Social and Governance (ESG) Report

American Savings Bank (ASB) released its first annual Environmental, Social and Governance (ESG) report, which highlights ASB’s ongoing efforts to sup...

-

March 03, 2023

Personal

March 03, 2023

Personal

5 Things to Know About Jumbo Loans

In home loan land, there are two big categories (aside from government loans): conforming loans and portfolio loans. There’s much more on that topic...

-

February 15, 2023

Personal

February 15, 2023

Personal

3 Mortgage Tips for Homeownership

At American Savings Bank (ASB), we’re committed to helping you achieve your dream of homeownership in Hawaii, whether you’re a first-time homebuyer or...

-

February 10, 2023

Personal

February 10, 2023

Personal

Paying a Mortgage vs. Paying Rent: What's the Difference?

You’re sitting at the kitchen table with another cup of coffee in the nighttime glow of your laptop. You’ve got a blank spreadsheet on your desktop, h...

-

February 03, 2023

News Releases

February 03, 2023

News Releases

American Savings Bank Announces 2022 Community Impact Contributions

American Savings Bank (ASB) announced its charitable contributions for the 2022 calendar year. In total, ASB donated more than $1.4 million to the com...

-

December 22, 2022

Community

December 22, 2022

Community

ASB Awards $140,000 to Winners of 2022 Bank for Education KeikiCo Business Plan Competition

American Savings Bank (ASB) announced the winners of its 2022 Bank for Education KeikiCo Business Plan Competition. Nearly 400 students grades 3 to 12...

-

November 21, 2022

Community

November 21, 2022

Community

American Savings Bank Celebrates Newly Renovated Hilo Branch

American Savings Bank (ASB) celebrated the completion of its Hilo branch renovation project at a private blessing ceremony on Monday, Nov. 21. The con...

-

November 20, 2022

News Releases

November 20, 2022

News Releases

ASB Distributes Thanksgiving Pies to 1,100 Teammates Across the State at “Pumpkin Pie Drive By”

American Savings Bank (ASB) hosted a statewide Thanksgiving drive-thru for its 1,100 teammates across the state on Sunday, Nov. 20, as part of its ann...

-

November 17, 2022

Personal

November 17, 2022

Personal

How to Start Saving Money for a House

When you spend your leisure time flipping through Zillow® and scrolling around decor inspo on Instagram, it can seem like actually saving up enough mo...

-

November 08, 2022

Personal

November 08, 2022

Personal

What Are Mortgage Points?

Mortgage points are one of the most often-referenced (and most confusing) parts of the mortgage conversation. Mark James, vice president and execut...

-

November 01, 2022

Personal

November 01, 2022

Personal

Tips on Taking Out Private Loans for College

Resources and content provided by College Ave Student Loans If you’re planning on going to college, you might need to take out private student loan...

-

November 01, 2022

Personal

November 01, 2022

Personal

Student Loan Credit Pre-Qualification

Resources and content provided by College Ave Student Loans “Will I be approved? What rates can I expect?” These thoughts have probably run through...

-

October 31, 2022

Personal

October 31, 2022

Personal

What is a Private Student Loan Cosigner? And Why Do I Need One?

Resources and content provided by College Ave Student Loans When it comes to the total cost of college, a private student loan can help fill i...

-

October 27, 2022

Personal

October 27, 2022

Personal

Banking is Easy and Convenient with ASB’s ATMs

At American Savings Bank (ASB), we’re always looking for ways to make banking easy and convenient for customers. Valerie Wada, branch manager at the K...

-

October 25, 2022

Personal

October 25, 2022

Personal

ASB Teammates Volunteer Across the State on National Make a Difference Day

American Savings Bank (ASB) teammates on four islands came together on Saturday, Oct. 22, which is National Make a Difference Day, to bring real impac...

-

September 22, 2022

News Releases

September 22, 2022

News Releases

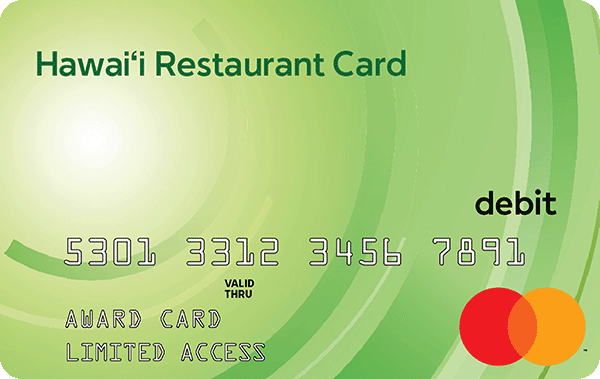

ASB Donates $129,000 of Unused Hawaiʻi Restaurant Card Business Holiday Card Funds to Three Local Nonprofits

American Savings Bank (ASB) announced it is donating $129,000 in unused funds from the Hawaiʻi Restaurant Card (HRC) Business Holiday Card program. Th...

-

September 07, 2022

News Releases

September 07, 2022

News Releases

ASB Supports Honolulu Little League World Series Champions with $12,000 Donation and a Two-Day Celebration

American Savings Bank (ASB) proudly supported the Honolulu Little League World Series (HLLWS) team in their quest to become this year’s Little Leagu...

-

July 29, 2022

Personal

July 29, 2022

Personal

5 Ways to Protect Your Money During Inflation

You may not be able to control rising gas prices or the volatility of the stock market, but now is the perfect time to take control of your finances s...

-

July 12, 2022

Personal

July 12, 2022

Personal

How to Buy a Home Despite High Interest Rates

Don’t let rising interest rates and an uncertain market environment deter you from making your homeownership dreams a reality. Michelle Luxton, vice p...

-

July 06, 2022

Personal

July 06, 2022

Personal

What Is a Parent Loan?

Resources and content provided by College Ave Student Loans A parent loan is money a student’s parent or guardian borrows to help pay for...

-

June 29, 2022

Personal

June 29, 2022

Personal

Prepare for Rising Mortgage Rates: Tips for Home Owners, Home Buyers and Investors

Market volatility and rising mortgage interest rates can cause uncertainty for home owners and those looking to buy, but with the right tools, resourc...

-

June 29, 2022

Personal

June 29, 2022

Personal

Student Loan Interest Rate vs. APR: What's the Difference?

Resources and content provided by College Ave Student Loans A student loan interest rate and a student loan annual percentage rate (APR) are simila...

-

June 28, 2022

Personal

June 28, 2022

Personal

How to Find the Right Mortgage For You

With so many financing options available, shopping for a mortgage in today’s competitive real estate market requires experience and expertise. Tha...

-

June 27, 2022

Personal

June 27, 2022

Personal

Student Loans 101: How Do Student Loans Work?

Resources and content provided by College Ave Student LoansIf you’re thinking about taking out a student loan to help pay for college, you might be na...

-

June 15, 2022

News Releases

June 15, 2022

News Releases

American Savings Bank Donates More Than $360,000 to Help Nonprofits and Community Recover From Pandemic

American Savings Bank's (ASB) 2022 Kahiau Giving Campaign raised $362,043, which will allow local community organizations to continue providing critic...

-

June 07, 2022

Business

June 07, 2022

Business

Quick Tip Tuesday: Expand Your Business by Offering More Ways to Pay

Digital technology has given customers a lot more flexibility in how they can pay and has also made the process significantly less complicated for bus...

-

May 31, 2022

Community

May 31, 2022

Community

NASA Astronaut Visits Hawaii Schools and Teaches Students to Dream Big

NASA Astronaut Dr. Michael Barratt visited three of American Savings Bank’s (ASB) Bank for Education Ohana Schools to talk to students grades K-5 abou...

-

February 18, 2022

News Releases

February 18, 2022

News Releases

American Savings Bank Announces 2021 Community Impact Contributions

American Savings Bank (ASB) announced its charitable contributions for the 2021 calendar year. In total, more than $1.5 million was donated to the com...

-

November 29, 2021

Business

November 29, 2021

Business

What a Business Credit Card Can Do for You

As a business owner, managing your cash flow is probably one of your biggest priorities. Many business owners find that they need extra cash to cove...

-

November 15, 2021

Personal

November 15, 2021

Personal

Credit Cards vs. Debit Cards - What's the Difference?

Credit and debit cards often look nearly identical at first glance. When someone pulls a card out in the checkout line, you may not know if they’re us...

-

November 09, 2021

Personal

November 09, 2021

Personal

Choosing the Right Credit Card for You

Are you in the market for a new credit card? With all the options available, it’s hard to know which one is right for you. At American Savings Bank, w...

-

October 18, 2021

Community

October 18, 2021

Community

#ASBPride: Manaola’s Story – The Search for Happiness

At American Savings Bank, we embrace and support customers and teammates from all backgrounds and sexual orientations. This diversity provides us with...

-

October 14, 2021

Community

October 14, 2021

Community

#ASBPride: Elisia’s Story – Returning Home with Pride

American Savings Bank is committed to creating a diverse, respectful and inclusive company for our teammates and customers. We want people from all wa...

-

October 13, 2021

Personal

October 13, 2021

Personal

Be Aware of Ransomware

Ransomware is a form of malware designed to hold a victim’s files and device hostage until they’ve paid the demanded ransom. We’re here to help you le...

-

October 08, 2021

Personal

October 08, 2021

Personal

Step Up Your Game with These Cybersecurity Tips

With October being National Cybersecurity Awareness Month, Levi Carias, Director of Information Security, joins HI Now Daily to share tips and onlin...

-

October 01, 2021

Community

October 01, 2021

Community

#ASBPride: John's Story - Embracing Your Pride

At American Savings Bank, individuals from all backgrounds, interests and sexual orientations are celebrated and supported. It’s important that we cre...

-

September 09, 2021

Community

September 09, 2021

Community

Free Vaccination Clinics at Aala Park on Sept. 12 and Oct. 3

ASB is committed to doing our part to stop the spread of COVID-19 in the community. We are partnering with Hawaii Pacific Health to host two FREE COVI...

-

August 30, 2021

Personal

August 30, 2021

Personal

Getting Started with Clean Energy Financing

More and more homeowners in Hawaii are choosing to go green when powering their homes. Installing solar or other clean energy systems to power your ho...

-

August 26, 2021

Personal

August 26, 2021

Personal

Boost Your Financial Health – Take Our Enhanced Financial Checkup!

Living in paradise isn’t cheap. On top of everyday expenses such as buying groceries and filling up gas, it may seem impossible to save enough money t...

-

August 23, 2021

Personal

August 23, 2021

Personal

Do You Have Enough Home Equity in Your Home to Refinance?

Do you want to refinance your mortgage? Whether you want to lower your interest rate or get rid of mortgage insurance, you’ll likely need to have equi...

-

August 09, 2021

News Releases

August 09, 2021

News Releases

American Savings Bank Opens Kapaa Digital Center

American Savings Bank held a blessing ceremony today at its Kapaa Digital Center, located at 4-831 Kuhio Highway, Suite 150. This is the fourth and fi...

-

July 28, 2021

Personal

July 28, 2021

Personal

Detect and Deflect Identity Theft

Identity thieves are continuously finding new ways to steal your information, but we can help you remain one step ahead and avoid their tricks. Identi...

-

July 26, 2021

Personal

July 26, 2021

Personal

How to Calculate the Equity in Your Hawaii Home

Your home’s equity is the difference between what you owe on your mortgage and what your home is currently worth. In Hawaii, many homeowners decide to...

-

July 22, 2021

Personal

July 22, 2021

Personal

Budgeting Tools to Help You Get Started

Do you want to have more control over your finances? Are you looking for a way to make reaching financial goals easier? There’s no magic wand when i...

-

July 16, 2021

Community

July 16, 2021

Community

Meet Our Newest Lo‘i Gallery Artists

American Savings Bank’s Lo‘i Gallery is proud to introduce three new talented artists, each offering a unique perspective of and homage to the peopl...

-

June 22, 2021

Personal

June 22, 2021

Personal

Breaking Down Different Types of Bank Accounts

Opening a bank account is one of the most important decisions you can make, so it's important to have all the facts. Lance Masuda, Director of Custome...

-

June 10, 2021

Personal

June 10, 2021

Personal

Online Banking vs. Traditional Banking: What's the difference?

The rise of technology in recent years has also led to new ways to bank — online via web browsers and smartphone applications. Online banking has beco...

-

June 01, 2021

Community

June 01, 2021

Community

ASB Is Proud to Celebrate National LGBTQ Pride Month

Happy National LGBTQ Pride Month! We’re proud to support the LGBTQ community all year long – including during National LGBTQ Pride Month every June an...

-

May 27, 2021

Personal

May 27, 2021

Personal

Comparing Mortgage Rates in Hawaii

Shopping for a home in Hawaii? Comparing mortgage rates is an important step in the home buying process. A lower interest rate could potentially sav...

-

May 17, 2021

Business

May 17, 2021

Business

The Ins & Outs of Business Loans

Are you a business owner? A business loan can help you to cover unexpected expenses, explore a new market or grow your company. No matter what your dr...

-

May 14, 2021

Business

May 14, 2021

Business

How to Save for Your Business

Owning your own business is exciting, but navigating the financial pieces can be challenging. Separating your business and personal expenses can hel...

-

May 10, 2021

Personal

May 10, 2021

Personal

Managing Debt in College and Beyond

The cost of higher education continues to be on the rise, with student loan debt becoming increasingly common among younger generations. Learning ho...

-

May 06, 2021

News Releases

May 06, 2021

News Releases

American Savings Bank President and CEO Rich Wacker Announces His Departure; Executive Vice President of Operations Ann Teranishi Named as Wacker’s Successor

American Savings Bank (ASB) announced today that President and Chief Executive Officer Rich Wacker will leave the company to pursue other interests. T...

-

May 06, 2021

Personal

May 06, 2021

Personal

Tips to Manage Your Credit

Understanding your credit score and figuring out how to improve your credit may sometimes feel daunting, but it’s something that’s necessary, as it ca...

-

May 03, 2021

Business

May 03, 2021

Business

Benefits of a Business Banker

Running a small business often means wearing many hats: you might be the founder, head of marketing, human resources manager and IT department of your...

-

April 28, 2021

Personal

April 28, 2021

Personal

Get to Know Personal Loans

Do you have a major purchase coming up, need to pay off debt or have an unexpected expense? A personal loan could help you to cover these costs by spr...

-

April 26, 2021

Personal

April 26, 2021

Personal

Armor Up Against Identity Fraud

Fraudsters these days are more conniving and persuasive than ever before. But, you can keep your identity and your finances secure all year round by s...

-

April 23, 2021

Personal

April 23, 2021

Personal

Investing in Your Financial Future

Investment planning is often one of the most stressful parts of planning for your financial future. You might be worried about potential market volati...

-

April 12, 2021

Personal

April 12, 2021

Personal

Understanding Interest Rates

You might have heard about interest rates but do you really know what they are and how they can help your finances? You might know that interest is th...

-

April 09, 2021

Personal

April 09, 2021

Personal

Using a Mortgage Calculator

Are you thinking of buying a home in Hawaii? Whether you’re a first time home buyer or are seeking to downsize in retirement, estimating your mortgage...

-

April 01, 2021

Personal

April 01, 2021

Personal

Celebrate Financial Literacy Month with These Useful Tips

April marks National Financial Literacy Month – a time when financial institutions like American Savings Bank help you to learn more about how you can...

-

March 30, 2021

Community

March 30, 2021

Community

ASB Stands with Asian American and Pacific Islanders

We are deeply troubled and saddened by the rise in verbal harassment, senseless mistreatment and violent hate crimes targeted at Asian Americans and P...

-

March 26, 2021

Other

March 26, 2021

Other

10 FAQS About Our Current Economy

The COVID-19 pandemic has made many unforeseen impacts on the United States economy, from nationwide unemployment to the affects it has had on trave...

-

March 18, 2021

News Releases

March 18, 2021

News Releases

ASB Earns Great Place to Work® Certification

This month, American Savings Bank was officially certified a Great Place to Work®, a designation awarded to the top companies around the world...

-

March 17, 2021

Community

March 17, 2021

Community

Meet Our Newest Lo‘i Gallery Artists

After a brief hiatus, ASB’s Lo‘i Gallery is back with three talented local artists, each representing a unique medium inspired by the people and natur...

-

March 10, 2021

Other

March 10, 2021

Other

Are you working from home? Here's how to save money while doing so

The COVID-19 pandemic has led many workplaces around the world to transition employees to remote work. While working from home can be an exciting chan...

-

February 24, 2021

Personal

February 24, 2021

Personal

Saving at Any Age

Saving is an important step toward overall financial health. From a child’s first account to retirement planning, good savings habits can help you t...

-

February 17, 2021

Personal

February 17, 2021

Personal

Why you should get life insurance early

Life insurance isn’t something young adults consider an immediate need. You might understand the benefit of having a life insurance policy when you’re...

-

January 26, 2021

Community

January 26, 2021

Community

Our Community Impact in 2020

2020 was a challenging year for many, with the drastic impacts the COVID-19 pandemic had on the economy and our local community. Many individuals an...

-

January 12, 2021

Personal

January 12, 2021

Personal

Making Home Loans Easy – Our New Online Mortgage Application

From shopping to schoolwork, much of what we normally do in person has gone digital due to the pandemic. Now, with the latest technology from Americ...

-

January 11, 2021

Personal

January 11, 2021

Personal

How to Deal with the Financial Impacts of a Job Loss or Pay Cut

Unemployment is at an all-time high due to economic impacts of the COVID-19 pandemic. In August 2020, Hawaii had the country’s highest “insured unempl...